Understanding Your Needs as a Parent or Educator

Whether you are a parent, a homeschool educator, or a traditional teacher, if you are reading this article, you are probably aware of a basic dilemma: traditional methods for teaching teens about money often don’t stick. let's first discuss these challenges:

What Is Beyond Personal Finance?

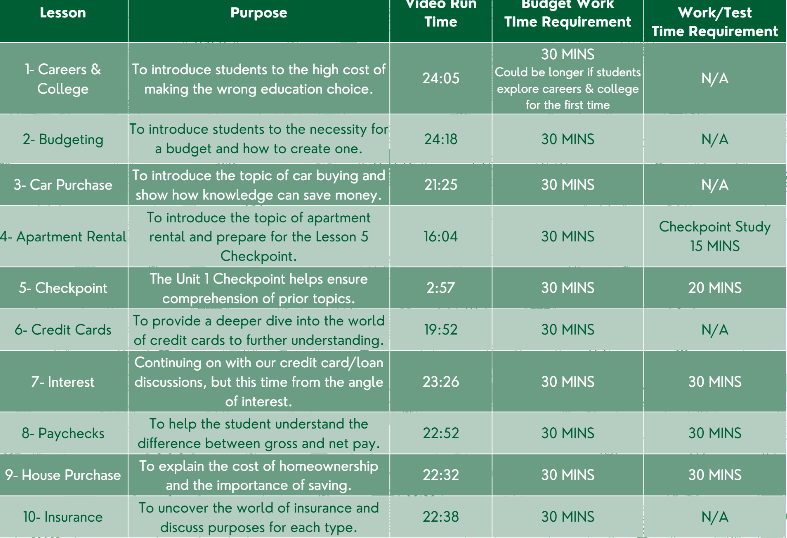

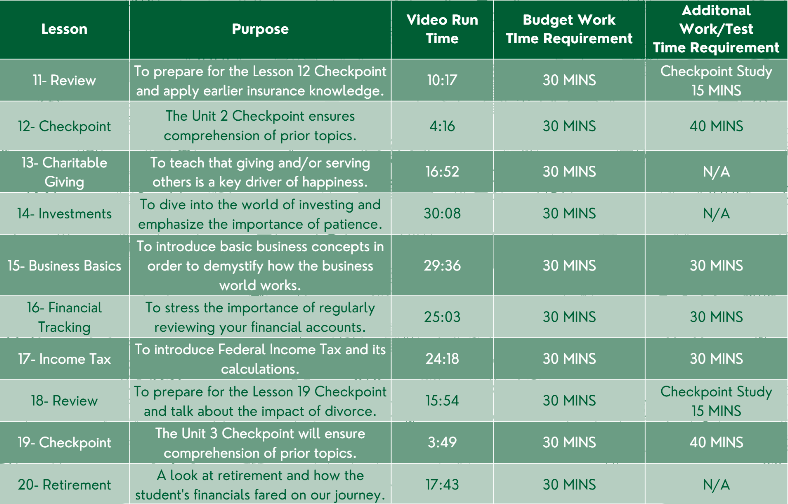

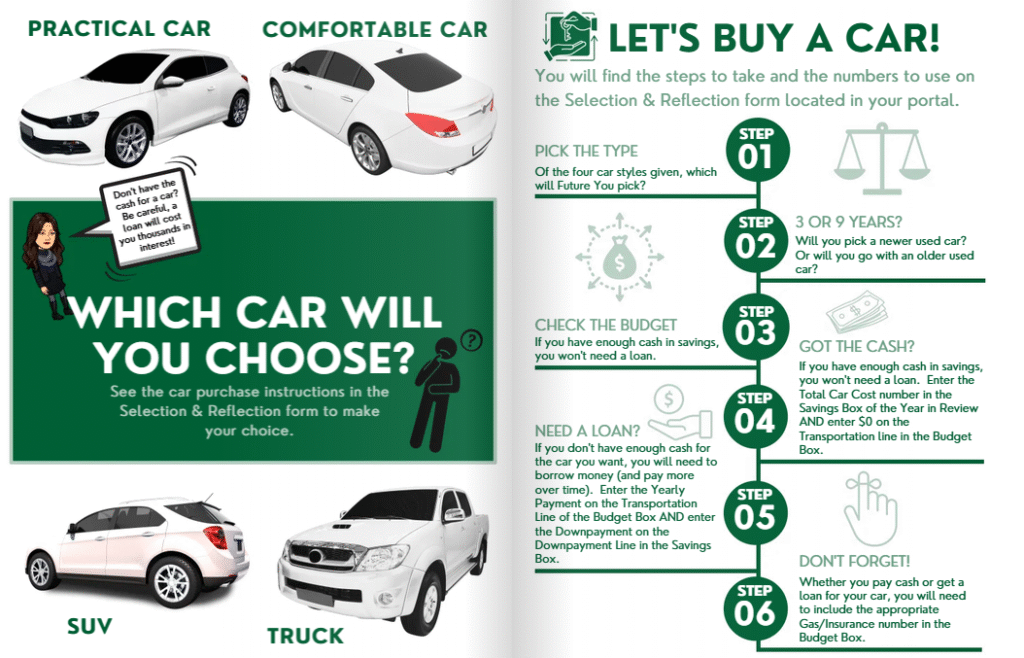

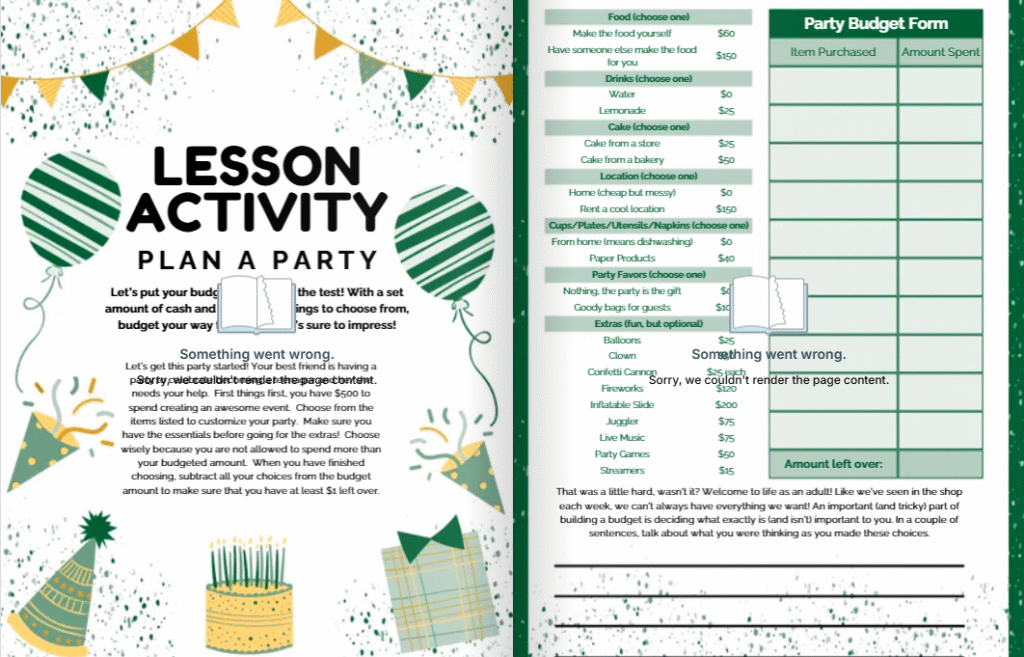

Beyond Personal Finance is a curriculum (choice based) developed by Charla McKinley to teach teens most important things about money management, starting with college and career planning and continuing on to marriage, buying a house, managing unemployment, paying tax on income, monitoring investments and other important factors of life that influence money. Check the below link to view class introduction video.

About the Course Creater

Charla McKinley is creator of “Beyond Personal Finance”. She is a University of Texas graduate, having finished with a degree in Finance and is a Certified CPA having more than 25 years of experience in the corporate and private sector. Her profound financial background coupled with her interest in young education made her create this interactive curriculum especially to the teenagers. McKinley was motivated by the fact that most financial education programs are geared towards adults that are already in a poor financial situation, and teens can hardly relate to the content. She calls Beyond Personal Finance a "smash-up of Dave Ramsey and the Game of Life," together with sound financial concepts presented in an exciting, game-show type style that appeals to the younger students.

Student Readiness

- My teen is able to complete online assignments and course work independently [Yes/No].

- My teen likes to make decisions and to observe the outcomes [Yes/No].

- My teen has simple mathematics knowledge (decimals, percentages, simple algebra) [Yes/No].

- My teen is keen to make his life better with good financial planning [Yes/No].

- A teenager is capable of dealing with appropriate financial principles [Yes/No].

Family/Classroom Fit

- We have stable internet and proper technology [Yes/No].

- My teens like to make decisions and to observe the outcomes [Yes/No].

- We can give 1-2 hours a week to this curriculum [Yes/No].

- The 150 dollars price is affordable to our education budget [Yes/No].

- An adult is available for further discussions with Teen [Yes/No].

- We would choose a complete curriculum rather than a fragmented resource [Yes/No].

Educational Goals

- We want real world practical financial skills, not only conceptual information [Yes/No].

- We prefer action and simulation-based learning methods [Yes/No].

- We need a complete curriculum, not add-ons or supplemental resources [Yes/No].

- We want to make our teen ready for college and early adult financial challenges [Yes/No].

- We want our teen to focus on personal finance rather than broader economics [Yes/No].

Alternative Considerations

- We have checked the free options and they are not sufficient and good enough [Yes/No].

- We choose self-contained curricula instead of the volunteer or educator-based ones [Yes/No].

- We desire something that is targeted to the teenage group and not modified adult content [Yes/No].

- We require flexibility in pace and time [Yes/No].

Final Decision

- If the answer of majority of questions is “Yes”, Beyond Personal Finance will be a worthwhile investment to your teenage finance education. The strengths of the program suit your needs and situation.

- In case answer of a few of the questions is “Yes”, we recommend trying a free version first, or check the possibility of your school and then may be you can go for Beyond Personal Finance. Similar programs are provided in the district. You can also look at single modules with other providers.

- In case answer of few questions is “Yes”, Beyond Personal Finance might not be the most suitable one. Think of more formal options like Foundations in personal finance course such as those offered by Dave Ramsey or a volunteer financial literacy mentor in the city.